by Mr. Kirill Savrassov

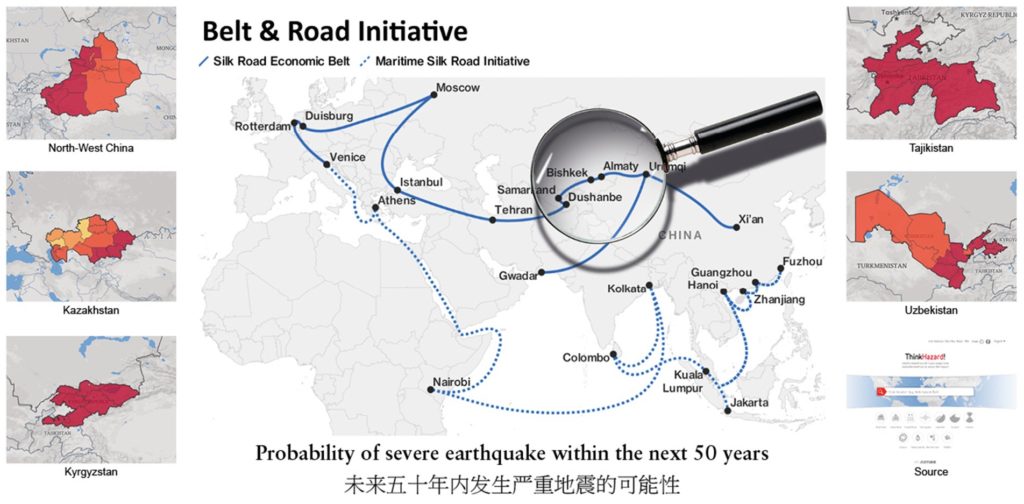

Countries in Central Asia and Eastern Europe that have been recipients of Chinese investment via projects associated with its Belt and Road Initiative (BRI) should use parametric sovereign cat bonds to insure themselves against the risk of natural disasters.

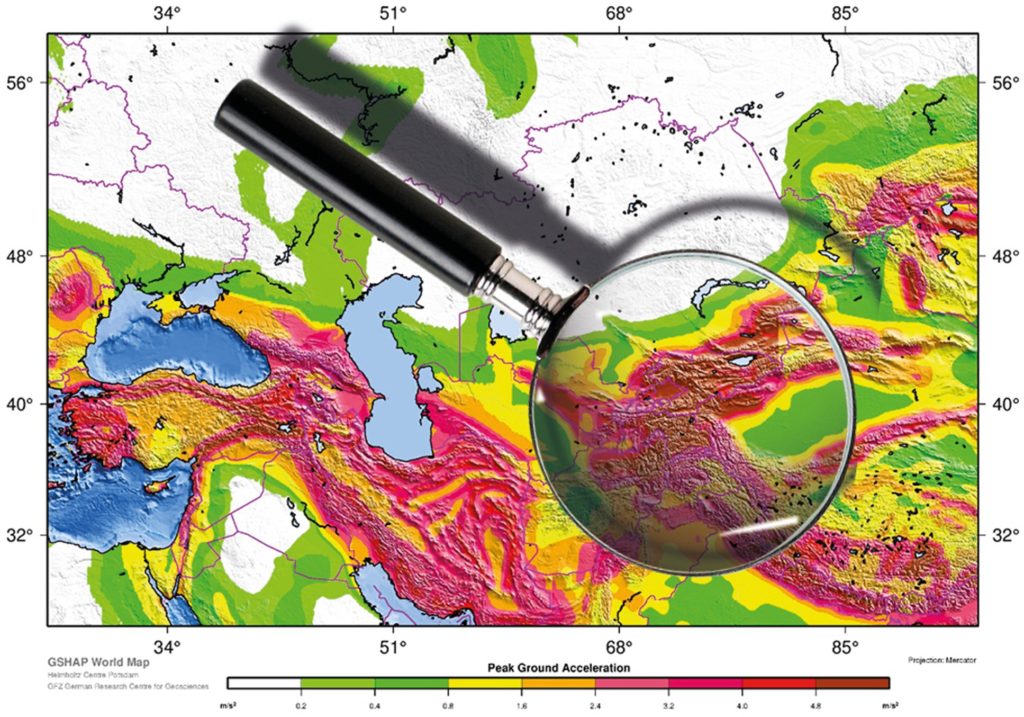

Belt and Road Initiative has created an even greater need for comprehensive protection solutions across Central Asia and Eastern Europe as China has spent tens of billions of dollars in infrastructure across the region but practically none of it is properly insured against physical damage, despite the region being at high risk of natural disasters with earthquakes in particular.

In countries such as Uzbekistan, Kazakhstan or Tajikistan it is not a question of if an earthquake will hit, but when—and how devastating it will be. In Western Balkans that is prone to earthquakes itself there is an additional threat of massive floods as climate change consequences.

This argument has a historical proof with just few examples to mention: Almaty (1911), Ashgabad (1948), Tashkent (1966) & Spitak (1988) when earthquakes brought huge economic and infrastructural damage. The 2014 Balkan floods caused damage and losses equivalent to nearly 5% of Serbia’s GDP and nearly 15% of Bosnia and Herzegovina’s GDP, with recovery needs straining government resources. In Macedonia in 2015 and 2016 heavy flooding caused major damage to roads, bridges and water management infrastructure, interrupting transport and economic activities across the nation.

So a natural disaster could devastate much of the infrastructure that China has helped to develop in the region via the BRI. If such a project is built but then destroyed by an earthquake or flood the host country will still owe China the money for the loans, without reaping the benefits from the infrastructure investment.

Emerging markets in general are vulnerable to the impact of natural disasters. According to Swiss Re, there is 35 % level of catastrophe risk coverage in advanced economies versus only 6 % in emerging economies.

While the insurance gap is a huge problem everywhere, the problem is far bigger for BRI transit countries between north-west China and Western Europe.

Extremely low insurance penetration, market underdevelopment and in some cases protectionism in the form of market access restrictions for international players or unnecessary intermediation in the form of local state reinsurers, make insurance unaccountable at the macro level, and unfold the necessity for alternative disaster risk transfer strategies and instruments.

Increasing insurance penetration is a good goal, but it’s not enough over the long term, so emerging markets governments across the world are therefore looking for innovative ways to increase their access to finance to enable disaster response, recovery, and rebuilding.

Out of available options, parametric sovereign cat bonds are the most logical and effective way for emerging markets to resolve their risk financing challenges.

In fact they are the only instrument that realistically will work because geopolitical fragmentation makes regional pooling arrangements impossible in Eastern Europe and Central Asia, while World Bank Contingent Credit instruments are too political. China and Russia’s influence over this region is important, while the World Bank may seem dominated by the US ; so parametric bonds solution remains neutral and therefore pragmatic option.

It is a warm market welcome for the steps taken by the Singapore Monetary Authority to grow its ILS business, which is fully sponsored by the Singapore government, and it is predicted Hong Kong will compete with Singapore for this business, encouraging growth of ILS in Asia and globally.

This should raise the profile of these innovative insurance products and embolden regional governments to use them to ensure they have adequate insurance coverage in case of natural disasters.

An important factor in favor of potential sovereign cat bonds in the region is an intra-class diversification for investment portfolios.

The stable appetite for ILS as uncorrelated asset class that institutional investors experience is concentrated on North American exposures. There is, therefore, a potential for intra-class diversification, and any new territory, especially the one yet be explored, shall attract big interest from investors’ circle as these options bring significant diversification element into their existing allocations/ILS portfolios.

Also, generally speaking, the overall performance of the ILS as asset class over the COVID-19 market volatility showed its bespoke value for uncorrelation purposes whereby it acted as almost defensive assets with only insignificant outflow in catastrophe bonds but only as investors were looking to free some resources to use in other affected areas.

So, there are no doubts that having ILS in the portfolios and different strategies will allow any asset manager to have some pure liquid and uncorrelated allocation. Moreover, investments into such bonds will act as indirect support and blanket protection of BRI critical infrastructure if Chinese institutional investors allocate for it.

The performance of the World Bank Pandemic Bond throughout the era of COVID-19 shows that parametric sovereign bonds in general are a great idea. Although there have been some reasonable criticisms of its performance and the structure may need to be adjusted and recalibrated, but de facto it worked so the proof of concept is there. Just some fine-tuning is required.

Generally speaking, the work done by the United Nations and international financial institutions to encourage governments to address the disaster risk finance at the right level is priceless. These efforts will lead to sustainability and macro-economic stability of developing nations in the face of devastating natural catastrophes.

The emergence of a healthy market for parametric sovereign cat bonds can be a reality within the next five to seven years. There needs to be just one deal and then there will be a domino effect. Things can happen very quickly once the logic is accepted.

To give an example – in the 1990s there was no market for international auditing in the former Soviet Union—people were happy to use local standards and companies. Even banks were not interested. But as trade with the west increased, people recognised the need to adhere to international standards, and now every big company uses them.

It took two decades for the market to go from one extreme to the other. For sure it can be the same with parametric sovereign bonds.

Mr. Kirill Savrassov, is an ILS and Sovereign Disaster Risk transfer specialist.

This is a revised article that first appeared in Intelligence Insurer 2020 Monte Carlo Today Magazine on September 17, 2020.

The views expressed in this article are those of the author, and do not necessarily reflect the views of OBOReurope.

Share the post "The BRI and the need for its transit infrastructure protection against natural disasters"

Pingback:The BRI and the need for its transit infrastructure protection against natural disasters | Phoenix CRetro

Pingback:ILS increasingly attractive in the face of COVID-19 | Phoenix CRetro

Pingback:China’s Belt and Road Initiative could kick-start ILS in Asia | Phoenix CRetro

Pingback:China Daily: Governments and institutions bet big on CAT bonds | Phoenix CRetro

Pingback:La BRI et la protection des infrastructures contre les désastres naturels | Phoenix CRetro

Pingback:参数化主权巨灾债券是“一带一路”的保险方式 | Phoenix CRetro

Pingback:Governments and institutions bet big on CAT bonds | Phoenix CRetro

Pingback:Parametric sovereign cat bonds: the way to insure the Belt and Road | Phoenix CRetro

Pingback:政府和机构指望巨灾债券 | Phoenix CRetro

Pingback:中国的“一带一路”倡议会将启动亚洲的保险连结证券 | Phoenix CRetro