by Toby Pughe FCII and Kirill K. Savrassov

With the BRI, new infrastructure have been constructed. But natural disasters can threaten large infrastructure projects and create financial turmoil in developing countries along the new Silk Road. Insurance-Linked Securities can mitigate this risk, but local authorities need to know more about this tool.

The protection gap, the difference between economic and insured losses, is a damning reflection on both the insurance market and those responsible for managing risk. Protection gaps exist in both developed and emerging markets, but where catastrophe risk coverage is around 35% in developed markets, it is just 6% in developing countries. According to AON, last year brought $268 billion of economic losses from natural disasters of which, just $97 billion was insured. Developing counties suffered a disproportionate share of uninsured losses, where damage sustained by businesses and governments are only increasing following a decade-long rise in natural catastrophes linked to climate change.

The long-term impacts of natural disasters are not predetermined, and the overall effect depends on the vulnerability of a country’s infrastructure, their access to disaster risk financing, and resilience. With inadequate insurance programs and a lack of alternatives, vulnerable countries (and sometimes even regions) have to rely on handouts from multilateral agencies and global development aid. However, such aid is reactive by nature, and payments can be slow to materialise. According to critics, there are also question marks around who the true beneficiaries of development aid are. Disasters do not just destroy homes, factories, and agricultural land in the short-term; they can annihilate years of economic growth.

Traditional indemnity insurance has been used for hundreds of years and to great effect. However, some of its limitations have started to surface over the last decade. For example, subjectivity around policy wordings has led to disputes in the courts spanning months, if not years, delaying disaster recovery and impacting affected parties further. The validity of traditional insurance is not being questioned by any means, but its suitability on a macro level in developing countries is. For example, in former Soviet Union countries, insurance in its traditional form is not suitable because sovereigns are responsible for critical infrastructure (therefore lack insurable interest).

When a natural disaster strikes, immediate steps need to be taken to protect survivors and provide them with temporary shelter, food, and water. Moreover, in the medium to long-term, homes, places of employment, and critical infrastructure such as schools and hospitals need to be rebuilt. In developed nations, government bodies such as FEMA in the USA typically act fast and provide these things. However, the same cannot be said for less developed markets. This is where Insurance-Linked Securities could make a significant contribution.

The renowned Chinese Belt and Road Initiative (BRI) is a perfect example where ILS could help transfer industrial and sovereign risk to the capital markets. China, through loans, has invested tens of billions of dollars in infrastructural development in Central Asia and other neighboring regions. Despite these regions having significant exposure to natural disasters, most of these new developments aren’t adequately insured.

The historical record of large disasters in the western BRI transit countries goes back to ancient Greece, where an earthquake in Crete destroyed Alexandria. More recently, in XX century earthquakes devastated Almaty (1911), Ashgabat (1948), Skopje (1963), Tashkent (1966), Bucharest (1977) and Spitak (1988). Floods, as well, has been an issue: from destruction of Pest in Hungary in 1838 to losses equating to 5-15% GDP of suffered countries during 2014-2016 Balkans Floods. In fact, close to 1/3 of the capitals of the ECIS countries have been at one time or another devastated by earthquakes or/and floods.

However, the issue isn’t only the physical damage from natural disasters themselves but also the repayment of loans. For example, if an earthquake in Central Asia destroyed a major logistics hub, not only will they suffer from business interruption, but also they still have to pay back the loans. Without adequate insurance, countries will have to foot the bill, and they might be worse off than before. The best way to avoid this scenario is to transfer their risk to the capital markets.

When Hurricane Maria struck the island of Puerto Rico in 2017, its people were without clean food and water for more than six months, 98% of buildings were either damaged or destroyed, and it took a further 11 months for power to fully restore on the island. If a parametric catastrophe bond programme or similar ILS solution was in place, capital could have flowed back into the economy sooner, and a return to their baseline would have been faster. Traditional insurance products, of course, still have a role to play, but ILS are perfectly suited to those who require fast injections of capital. This correlates with the United Nations’ argument that the speed of recovery really matters if a developing country is to minimise the long-term impacts of natural disasters on economic growth and productivity.

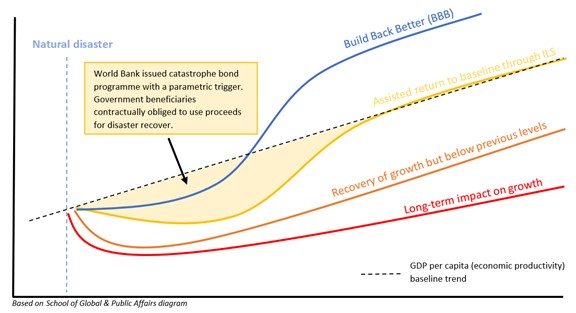

Furthermore, this type of disaster financing is far more efficient than traditional forms of insurance. Rather than waiting for loss adjusters and surveyors to assess the damage, ILS can provide immediate liquidity to governments that need it the most. In the diagram below, we have a countries baseline trend of economic growth. Common sense suggests that a destruction of capital will lead to an inability to produce goods and services, and growth will fall. The economy would recover, but given the long-term implications of damaged infrastructure and productivity, the trajectory of growth will be lower than before.

However, (and this is where ILS comes in) neoclassical economic growth theory would suggest that lower levels of capital might allow for higher productivity gains. By introducing a transparent, fast paying insurance-linked security like a catastrophe bond, economic growth and productivity could return to or exceed the baseline faster than if traditional insurance was in place. These capital flows help to address humanitarian crises, the rebuilding of infrastructure, and the creation of jobs. By stipulating that the bond proceeds must be spent on redevelopment projects, governments can focus on building back better and replacing old and weak infrastructure with buildings that conform to updated code.

So far, government pools such as the Caribbean Catastrophe Risk Insurance Facility (CCRIF) and Africa Risk Capacity (ARC) have illustrated the benefits of pooling regional risk and leveraging ILS. A recent example is the CCRIFs payment of $10.7m to Nicaragua after Tropical Cyclone Eta. Although this may seem a small amount in dollar terms, payment was made within 14 days. These fast injections of capital can often be the difference between life and death.

However, for the Eurasia transit countries, regional pools like the CCRIF and Pacific Alliance or World Bank contingent credit aren’t viable options because of the region’s geopolitical fragmentation. Underdeveloped insurance markets, low insurance penetration, and protectionism (restricted market access for international players) in several countries also make insurance placements a challenge at the macro level, unfortunately.

At the same time use of ILS for disaster risk transfer in the form of sovereign parametric catastrophe bonds is a neutral and feasible option, advantageous to beneficiaries and investors.

Catastrophe bonds are transparent, objective, and payouts are typically fast, making them ideal for critical infrastructure that a country might rely on to drive its GDP if disaster occurs. Furthermore, they can also help countries with a low credit rating that would typically struggle to source traditional financing or rely on slow/unreliable global development aid.

A better understanding of ILS can help traditional markets and governments transfer risk more efficiently. The lack of government understanding around ILS also does not help, so bridging the education gap is vital.

Multinational agencies like the World Bank and the United Nations Development Programme (UNDP) are doing an excellent job promoting products such as parametric insurance and instruments that transfer risk to the capital markets. However, their involvement alone is not enough. We believe that industry participants, associations, and, more importantly, academia need to join forces in a dedicated effort to educate local market participants, opinion leaders, and government officials to help them make better decisions.

Moreover, convergence between insurance and the broader capital markets is relatively straightforward in terms of legislation and local frameworks. If a country has already utilised the capital markets through sovereign bond issuance, it can do the same for disaster risk financing without any additional constraints.

Share the post "Narrowing the Education Gap and Insurance-Linked Securities (ILS)"

Pingback:Narrowing the Education Gap and Insurance-Linked Securities (ILS) – PHCRE: ILS Made Simple

Pingback:Mieux connaître les titres liés à l’assurance (Insurance-Linked Securities, ILS) – PHCRE: ILS Made Simple

Pingback:教育差距缩小与保险连结证券 – Fundamentals of ILS

Pingback:教育差距缩小与保险连结证券 – PHCRE: ILS Made Simple